Accounting Ratios

Aims:-

Accounting ratios are useful measurements with which to identify financial results which need further investigation. There are several results of a business which can be usefully measured using ratios. The main groupings are:-

In all cases, the figures concerned must be compared with other figures from:

Profitability (performance) ratios

These ratios measure the level of profitability of the business. the following are commonly used profitability ratios:-

1. Gross profit percentage

This ratio measures the gross profit as a percentage of sales (i.e. net sales or turn over)

Gross profit percentage (margin) = Gross Profit x 100

Net sales

2. Net profit percentage

This ratio expresses the net profit as a percentage of sales revenue and this ratio is most often used by firms to compare their profit with other firms.

Net profit percentage = Net profit X 100

Net sales

3. Return on capital employed

This ratio expresses the net profit as a percentage of capital invested

Return on capital employed (ROCE) = Net profit X 100

Capital employed

Capital employed can have different meanings. The most widely used formula for capital employed is as follows:

Capital employed = Capital on the closing date. (Total assets - Total liabilities)

In the case a limited company, it is the total of the shareholders’ funds.

Liquidity (solvency ratios)

These ratios measure the ability of a firm to pay its debts as they fall due.

1. Current (working capital ) ratio

This ratio compares the current assets with the current liabilities.

Current ratio = Current assets

Current liabilities

A ratio of 2:1 is considered to be a good standard, but it may vary depending upon the nature of the business and other organizations in the same line of business.

2. Acid test (quick ratio)

This ratio tests for insolvency – if a business has sufficient liquid resources ( quick assets) to meet its current liabilities. To calculate this ratio, closing stock should be removed from the current assets where the stocks are not likely to be sold very quickly.

Acid test ratio = Current assets – closing stock

Current liabilities

The standard for this ratio is 1:1, a lower ratio indicating insolvency

Use of assets (efficiency ratios)

1. Stock turn over (stock turn) ratio

This ratio shows how quickly the business sells its stock – how many times the stock ‘turns over” in a year.

The rate of stock turn over = Cost of sales

Average stock

Where, average stock = Opening stock + closing stock

2

If the rate increases, it may indicate efficiency is improving (sales are increasing) and if it reduces it may mean that the efficiency is deterioting (the business has too much stock because the sales are slowing down)

2. Debtors turn over ratio( Debtors collection period)

This ratio shows how long it is taking to collect debts from customers. The faster cash is collected from debtors, the better the cash flow of the business. It also shows the credit control policy of the business.

Debtors’ collection period = Debtors x 365 days ( or 52 weeks or 12 months)

Credit sales

3. Creditors turn over ratio (creditors payments period)

This ratio shows how quickly the business pays its creditors. A longer period indicates that the business is taking longer to pay its creditor and hence is holding on to cash which may lead the creditors to refuse to sell to the business.

Creditors payments period = Creditors x 365 days ( or 52 weeks or 12 months)

Credit purchases

It is also important to compare the creditors payments period with the debtors collection period - ideally, it should take longer to pay creditors than to collect monies from debtors.

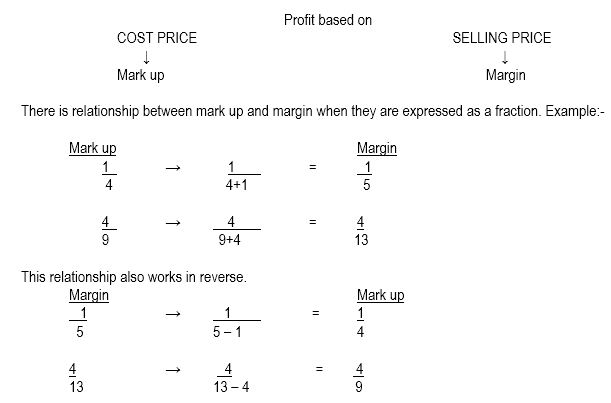

Relationship between Mark – up and Margin

Cost price + profit = Selling price.

Cost of sales + profit = Sales

Aims:-

- to explain the importance of the comparison of financial results

- to demonstrate the calculation of, and explain the usefulness of, the main accounting ratios

Accounting ratios are useful measurements with which to identify financial results which need further investigation. There are several results of a business which can be usefully measured using ratios. The main groupings are:-

- Profitability ratios (to measure the profitability of the business)

- Solvency ratios ( to measure the liquidity position of the business)

- Use of assets ratios ( to measure the efficiency of the business )

In all cases, the figures concerned must be compared with other figures from:

- previous periods of the same business

- other organizations of carrying on similar business

- plans and budgets

Profitability (performance) ratios

These ratios measure the level of profitability of the business. the following are commonly used profitability ratios:-

1. Gross profit percentage

This ratio measures the gross profit as a percentage of sales (i.e. net sales or turn over)

Gross profit percentage (margin) = Gross Profit x 100

Net sales

2. Net profit percentage

This ratio expresses the net profit as a percentage of sales revenue and this ratio is most often used by firms to compare their profit with other firms.

Net profit percentage = Net profit X 100

Net sales

3. Return on capital employed

This ratio expresses the net profit as a percentage of capital invested

Return on capital employed (ROCE) = Net profit X 100

Capital employed

Capital employed can have different meanings. The most widely used formula for capital employed is as follows:

Capital employed = Capital on the closing date. (Total assets - Total liabilities)

In the case a limited company, it is the total of the shareholders’ funds.

Liquidity (solvency ratios)

These ratios measure the ability of a firm to pay its debts as they fall due.

1. Current (working capital ) ratio

This ratio compares the current assets with the current liabilities.

Current ratio = Current assets

Current liabilities

A ratio of 2:1 is considered to be a good standard, but it may vary depending upon the nature of the business and other organizations in the same line of business.

2. Acid test (quick ratio)

This ratio tests for insolvency – if a business has sufficient liquid resources ( quick assets) to meet its current liabilities. To calculate this ratio, closing stock should be removed from the current assets where the stocks are not likely to be sold very quickly.

Acid test ratio = Current assets – closing stock

Current liabilities

The standard for this ratio is 1:1, a lower ratio indicating insolvency

Use of assets (efficiency ratios)

1. Stock turn over (stock turn) ratio

This ratio shows how quickly the business sells its stock – how many times the stock ‘turns over” in a year.

The rate of stock turn over = Cost of sales

Average stock

Where, average stock = Opening stock + closing stock

2

If the rate increases, it may indicate efficiency is improving (sales are increasing) and if it reduces it may mean that the efficiency is deterioting (the business has too much stock because the sales are slowing down)

2. Debtors turn over ratio( Debtors collection period)

This ratio shows how long it is taking to collect debts from customers. The faster cash is collected from debtors, the better the cash flow of the business. It also shows the credit control policy of the business.

Debtors’ collection period = Debtors x 365 days ( or 52 weeks or 12 months)

Credit sales

3. Creditors turn over ratio (creditors payments period)

This ratio shows how quickly the business pays its creditors. A longer period indicates that the business is taking longer to pay its creditor and hence is holding on to cash which may lead the creditors to refuse to sell to the business.

Creditors payments period = Creditors x 365 days ( or 52 weeks or 12 months)

Credit purchases

It is also important to compare the creditors payments period with the debtors collection period - ideally, it should take longer to pay creditors than to collect monies from debtors.

Relationship between Mark – up and Margin

Cost price + profit = Selling price.

Cost of sales + profit = Sales

Advantages of accounting ratios

- It helps to compare two or more business units.

- We can compare the results of a business over two periods.

- On the basis of ratios, the growth or the decline of the business can be understood very easily.

- To plan for the future.

- Only past events expressed in terms of money alone can be analysed.

- Different accounting methods give different results that cannot not be compared.

- No allowance is made for inflation, which makes comparison of results between different periods meaningless.

- Other non monetary and non financial factors are ignored (eg: staff relations, efficiency of the management, business location, environmental conditions etc...)

- Only like – with - like items can be compared (similar sized businesses, different periods for the same business, Plans and budgets.