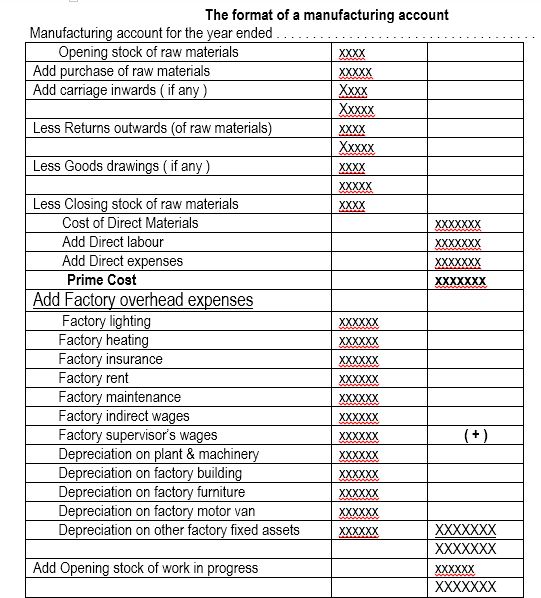

Manufacturing account

The businesses which produce and sell the items prepare the following accounts at the end of its accounting year:-

a. The Manufacturing account (to calculate the total cost of production)

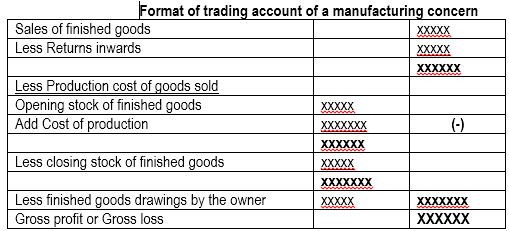

b. The Trading and profit & loss account (to find out the net profit or loss)

c. The balance sheet.(to show the financial position of the business)

The total cost of production = Prime cost + Factory overhead

The Prime cost = Direct material + Direct labour + Direct expenses

Direct material cost = Opening stock of raw materials + purchase of raw materials +

Carriage inwards – returns outwards – closing stock of raw materials.

Factory overhead expenses = All expenses related to the factory (indirect expenses)

In a manufacturing concern, usually there are three kinds of stocks:

Stock of Raw materials (the materials which are mainly used for production of the item)

Stock of Work in progress (the materials on which some work process have been completed)

Stock of Finished goods (The materials on which all the production processes are completed and ready for sale to the customers)

In the examination questions, the stock figures will be given separately.

The businesses which produce and sell the items prepare the following accounts at the end of its accounting year:-

a. The Manufacturing account (to calculate the total cost of production)

b. The Trading and profit & loss account (to find out the net profit or loss)

c. The balance sheet.(to show the financial position of the business)

The total cost of production = Prime cost + Factory overhead

The Prime cost = Direct material + Direct labour + Direct expenses

Direct material cost = Opening stock of raw materials + purchase of raw materials +

Carriage inwards – returns outwards – closing stock of raw materials.

Factory overhead expenses = All expenses related to the factory (indirect expenses)

In a manufacturing concern, usually there are three kinds of stocks:

Stock of Raw materials (the materials which are mainly used for production of the item)

Stock of Work in progress (the materials on which some work process have been completed)

Stock of Finished goods (The materials on which all the production processes are completed and ready for sale to the customers)

In the examination questions, the stock figures will be given separately.