THE FINAL ACCOUNTS OF A SOLE TRADER

The trading account, profit and loss account and the balance sheet are called final accounts. Usually, the final accounts are prepared at the end of an accounting period.

* Trial balance is the basis for preparing the final accounts.

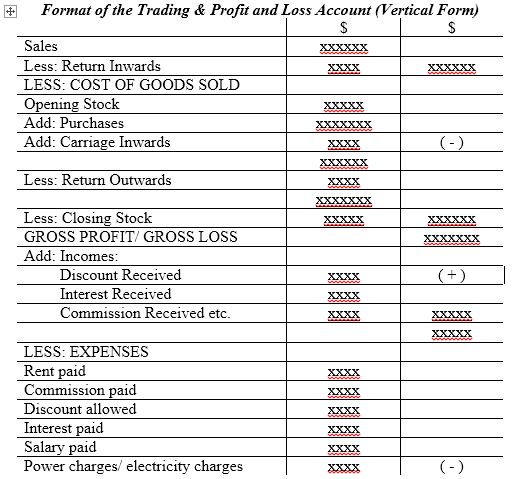

TRADING AND PROFIT & LOSS ACCOUNT

Gross Loss = Cost of goods sold – Net sales

Net Profit = Gross Profit + Incomes – Expenses

Net Loss = Expenses – Incomes – Gross Profit

Note:

Net sales = Total sales – Sales returns/ Return Inwards.

Cost of goods sold = Opening stock + Purchases + Carriage Inwards

– Return Outwards/ Purchase Returns – Closing Stock

The trading account, profit and loss account and the balance sheet are called final accounts. Usually, the final accounts are prepared at the end of an accounting period.

* Trial balance is the basis for preparing the final accounts.

TRADING AND PROFIT & LOSS ACCOUNT

- The purpose of preparing the trading account is to find out the gross profit or gross loss of the business during an accounting period.

- The purpose of preparing the profit and loss account is to find out the net profit or net loss of the business for an accounting period

Gross Loss = Cost of goods sold – Net sales

Net Profit = Gross Profit + Incomes – Expenses

Net Loss = Expenses – Incomes – Gross Profit

Note:

Net sales = Total sales – Sales returns/ Return Inwards.

Cost of goods sold = Opening stock + Purchases + Carriage Inwards

– Return Outwards/ Purchase Returns – Closing Stock

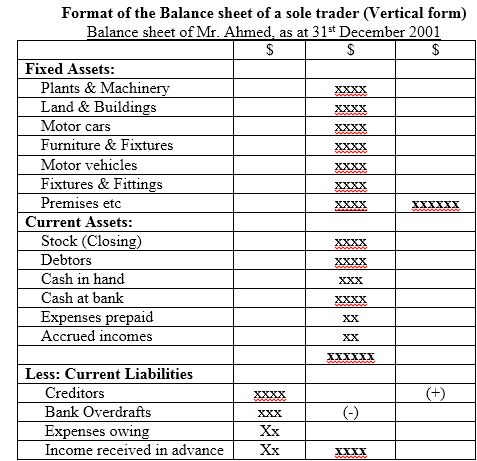

BALANCE SHEET

This is the statement of assets and liabilities of a business prepared on a particular date to show the financial position of a business. The Balance sheet is prepared after the preparation of the trading, profit and loss account.

This is the statement of assets and liabilities of a business prepared on a particular date to show the financial position of a business. The Balance sheet is prepared after the preparation of the trading, profit and loss account.

- The balance sheet is prepared with the account balances left after the preparation of the trading and profit & loss account.

- Usually, the trading account and the profit and loss account are prepared together. But the balance sheet is prepared separately.

The Final Accounts of a sole trader (With Adjustments)

The trading and profit & loss account and balance sheet prepared at the end of a year is known as Final accounts. While preparing the final accounts, there may be some items so far not adjusted. These items are to be adjusted in the final accounts for calculating the correct profit or loss of the business. The usual adjustments in the final accounts are:-

a. Expenses owing: - These are the expenses incurred during the year but not paid in cash. This amount will be paid in the near future (next year). The owing expense is to be added with the amount of same expense already paid given in the trial balance and it should be shown in the balance sheet

as a current liability.

The double entry for recording the expenses owing is

Debit Expenses account

Credit Expenses owing account

This expense is also known as outstanding expenses, expenses payable or expense payable.

b. Prepaid expense. :- This is the expense paid during the year for the benefit of the next year. The portion of the expense which is prepaid is to be deducted from the total expenses already paid during the year (given in the trial balance) and shown as current asset in the balance sheet.

The double entry for recording the prepaid expense is

Debit Prepaid expense account and

Credit Expense account

This expense is also known as expense paid in advance or unexpired expense

c. Accrued income:- The income earned during the year but not received in cash is known as accrued income. The amount of accrued income is to be considered as current year’s income and added

with the concerned income received during the year(given in the trial balance) and shown as a current asset in the balance sheet.

The double entry for recording the accrued income is:

Debit Accrued income account and

Credit Income account

The accrued income is also known as outstanding income.

d. Income received in advance:- This is the income received during the year for the services to be rendered during the next year. Since this income is not related to the current year, it should be deducted from the concerned income (given in the trial balance) and shown as a current liability

in the balance sheet.

The double entry for recording the income received in advance is:

Debit Income account and

Credit Income received in advance

This is also known as unexpired income.

e. Depreciation:- The part of the cost of a fixed asset that is consumed by a business during the period

of its use is known as depreciation. It is considered as an expense in the business therefore shown as an expense in the profit & loss account and deducted from the cost price of the concerned fixed asset in the balance sheet.

The double entry for recording depreciation is:

Debit Profit & loss account and

Credit Depreciation account

f. Bad debt:- The part of the amount of debtors which cannot be recovered is known as bad debt. It is an expense to be shown in the profit & loss account. If the bad debt appears in the trial balance, it is known as bad debt written off and shown in the profit & loss account only. If bad debt information appears among the adjustment points below the trial balance, then it should be shown as an expense in the profit & loss account and shown as a deduction from the debtors in the balance

sheet under the heading “current assets”.

The double entry for recording the bad debt is:

Debit Bad debt account and

Credit Debtors account

g. Goods drawings by the owner for his personal use:-

The amount of goods withdrawn by the owner for his personal use is to be considered as drawing. The double entry for recording the goods drawings is:

Debit Drawings account and

Credit Purchase account or sales account

The amount of goods drawings should be deducted form purchases and capital in the balance

sheet.

The trading and profit & loss account and balance sheet prepared at the end of a year is known as Final accounts. While preparing the final accounts, there may be some items so far not adjusted. These items are to be adjusted in the final accounts for calculating the correct profit or loss of the business. The usual adjustments in the final accounts are:-

a. Expenses owing: - These are the expenses incurred during the year but not paid in cash. This amount will be paid in the near future (next year). The owing expense is to be added with the amount of same expense already paid given in the trial balance and it should be shown in the balance sheet

as a current liability.

The double entry for recording the expenses owing is

Debit Expenses account

Credit Expenses owing account

This expense is also known as outstanding expenses, expenses payable or expense payable.

b. Prepaid expense. :- This is the expense paid during the year for the benefit of the next year. The portion of the expense which is prepaid is to be deducted from the total expenses already paid during the year (given in the trial balance) and shown as current asset in the balance sheet.

The double entry for recording the prepaid expense is

Debit Prepaid expense account and

Credit Expense account

This expense is also known as expense paid in advance or unexpired expense

c. Accrued income:- The income earned during the year but not received in cash is known as accrued income. The amount of accrued income is to be considered as current year’s income and added

with the concerned income received during the year(given in the trial balance) and shown as a current asset in the balance sheet.

The double entry for recording the accrued income is:

Debit Accrued income account and

Credit Income account

The accrued income is also known as outstanding income.

d. Income received in advance:- This is the income received during the year for the services to be rendered during the next year. Since this income is not related to the current year, it should be deducted from the concerned income (given in the trial balance) and shown as a current liability

in the balance sheet.

The double entry for recording the income received in advance is:

Debit Income account and

Credit Income received in advance

This is also known as unexpired income.

e. Depreciation:- The part of the cost of a fixed asset that is consumed by a business during the period

of its use is known as depreciation. It is considered as an expense in the business therefore shown as an expense in the profit & loss account and deducted from the cost price of the concerned fixed asset in the balance sheet.

The double entry for recording depreciation is:

Debit Profit & loss account and

Credit Depreciation account

f. Bad debt:- The part of the amount of debtors which cannot be recovered is known as bad debt. It is an expense to be shown in the profit & loss account. If the bad debt appears in the trial balance, it is known as bad debt written off and shown in the profit & loss account only. If bad debt information appears among the adjustment points below the trial balance, then it should be shown as an expense in the profit & loss account and shown as a deduction from the debtors in the balance

sheet under the heading “current assets”.

The double entry for recording the bad debt is:

Debit Bad debt account and

Credit Debtors account

g. Goods drawings by the owner for his personal use:-

The amount of goods withdrawn by the owner for his personal use is to be considered as drawing. The double entry for recording the goods drawings is:

Debit Drawings account and

Credit Purchase account or sales account

The amount of goods drawings should be deducted form purchases and capital in the balance

sheet.