Control Accounts

Control Accounts are the total accounts used for checking the arithmetical accuracy of each of ledger separately. The two most common control accounts are:

(i)The sales ledger control account (debtors ledger control a/c / total debtors a/c) and

(ii)The purchase ledger control account (creditors ledger control a/c/total creditors a/c)

A control account contains the same information as the individual ledger accounts which it controls, but in total.

Purposes of control accounts

Control Accounts are the total accounts used for checking the arithmetical accuracy of each of ledger separately. The two most common control accounts are:

(i)The sales ledger control account (debtors ledger control a/c / total debtors a/c) and

(ii)The purchase ledger control account (creditors ledger control a/c/total creditors a/c)

A control account contains the same information as the individual ledger accounts which it controls, but in total.

Purposes of control accounts

- To act as a check on the accuracy of the totals of the balances in the sales and purchases ledgers.

- To provide totals of debtors and creditors quickly when a trial balance is being prepared.

- To identify the ledger(s) in which errors have been made when there is a difference on the trial balance.

- To act as an internal check on the work of the sales and purchases ledger clerks – to detect errors and deter fraud, under the charge of a responsible person

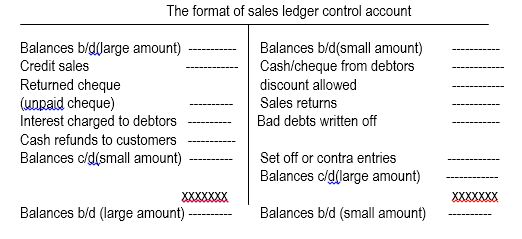

Sources of information for items appearing in the sales ledger control account

- Credit sales- sales day book – total.

- Returned cheques (unpaid cheques) – cash book- payments side/ bank statement.

- Interest charged to debtors- Interest received account.

- Cash or cheques from debtors – cash book-receipts side.

- Discount allowed – cash book (debit side) or discount allowed account.

- Sales returns – sales returns day book total.

- Bad debts written off – general journal or bad debts account.

- Set off or contra entries- general journal.

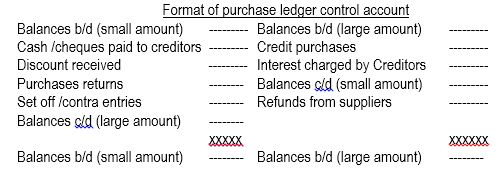

Sources of information for items appearing in the purchases ledger control account

a Credit purchases – purchases day book total

b. Interest charged by creditors – interest paid account.

c. Cash/cheque paid to creditors – cash book – payments side.

d. Discount received – cash book payment side or discount received account

e. Purchases returns – purchases returns day book total.

f. Set off or contra entries – general journal.

Set off / contra entries. Sometimes, the same person may be a debtor as well as a creditor for the business. At the end of the month, the smaller amount in his account from one ledger is transferred to his account in the ledger with large amount. The entry passed for recording this transfer is known as set off or contra entry. Key Points

a Credit purchases – purchases day book total

b. Interest charged by creditors – interest paid account.

c. Cash/cheque paid to creditors – cash book – payments side.

d. Discount received – cash book payment side or discount received account

e. Purchases returns – purchases returns day book total.

f. Set off or contra entries – general journal.

Set off / contra entries. Sometimes, the same person may be a debtor as well as a creditor for the business. At the end of the month, the smaller amount in his account from one ledger is transferred to his account in the ledger with large amount. The entry passed for recording this transfer is known as set off or contra entry. Key Points

- Control accounts are considered as total accounts.

- Debtors ledger control account is also known as sales ledger control account or total debtors account.

- Creditor’s ledger control account is also known as purchases ledger control account or total creditors account.

- Balance in sales ledger control account is the balance of debtors at the year end and balance in purchases ledger control account is balance of creditors.

- Cash sales and cash purchases are not recorded in the control accounts.

- The double entry to record set off from purchase ledger to sales ledger is to debit purchase ledger control account and credit sales ledger control account.

- Dishonoured cheque which was received from debtors is shown in the debit side of the sales ledger control account.

- Interest on overdue accounts charged from customers and refunds to customers for overpayments by them are shown on the debit side of sales ledger control account.

- Interest charged by suppliers and refunds received from suppliers for overpayments to them are recorded in the credit side of purchases ledger control account.

- Provision for bad debts is not included in sales ledger control account

- Small balance in a control account represents advance payments, overpayments etc.