Company Accounts

The capital of a limited company is divided into shares. A person can become the member of a company if he buys a share. Then he is known as the shareholder. If the shareholder has paid in full for the shares he has taken, his liability is limited to the nominal value of those shares only. When the company loses its assets, it cannot ask the shareholders to pay anything out of their private property in respect of the company’s losses. If the shareholder has paid partly only for the shares, he can be forced to pay the balance owing on the shares. In short, the liability of each member is limited to the nominal value of the shares he has taken. This is known as limited liability and the company is known as limited company.

Share capital (different meaning)

1. Authorized/registered/nominal share capital. This is the total of the share capital which the company is allowed to issue to the shareholders.

2. Issued share capital: This is the total of the share capital actually issued to the shareholders.

3. Called up capital: Where only part of the amounts payable on each share has been asked for, the total amount asked for on all the shares is known as the called up capital.

4. Uncalled capital: This is the total amount which is to be received in future, but which has not yet been asked for.

5. Calls in arrears: The total amount for which payment has been asked but has not been paid by share holders.

6. Paid up capital: This is the total of the amount of share capital which has been actually paid by the shareholders.(Paid up capital = Called up capital – Calls in arrears)

Key points

1. Debentures- loan to the company from the public carrying fixed rate of interest.

2. Dividend: The profit that is being distributed to shareholders is called dividends.

3. Debenture interest: This is the interest paid on debentures to the debenture holders. This is an expense to be charged in the profit and loss account and if it owes it is known as a current liability in the balance sheet.

4. Ordinary shares: Shares entitled to dividend after the preference shareholders have been paid their dividends.

5. Preference shares: Shares that are entitled to an agreed rate of dividend before the ordinary shareholders receive anything.

6. Reserves: The transfer of apportioned profits to accounts for use in future.

7. Directors remunerations: This is the remuneration given to the directors and an expense to be shown in the profit and loss account.

8. Interim dividend: The dividend paid to the shareholders in between two annual general meetings.

It is shown in the profit & loss appropriation account only.

9. Proposed dividend: This dividend agreed by the board of directors but not paid. It is deducted from the profit & loss appropriation account and shown as a current liability in the balance sheet

10. Dividend is calculated on the paid up capital only.

11. For preference shares prefixed rate of dividend is paid.

E.g.: 7% Preference shares ----------------- rate of dividend is 7%

Therefore, preference dividend = Issued preference share capital x rate (%) / 100

12. For ordinary shares:

if dividend is paid as percentage of capital

Dividend = Issued ordinary share capital (nominal value) x rate (%) / 100

If dividend is payable per share:

Dividend = Number of ordinary issued shares x dividend per share

The capital of a limited company is divided into shares. A person can become the member of a company if he buys a share. Then he is known as the shareholder. If the shareholder has paid in full for the shares he has taken, his liability is limited to the nominal value of those shares only. When the company loses its assets, it cannot ask the shareholders to pay anything out of their private property in respect of the company’s losses. If the shareholder has paid partly only for the shares, he can be forced to pay the balance owing on the shares. In short, the liability of each member is limited to the nominal value of the shares he has taken. This is known as limited liability and the company is known as limited company.

Share capital (different meaning)

1. Authorized/registered/nominal share capital. This is the total of the share capital which the company is allowed to issue to the shareholders.

2. Issued share capital: This is the total of the share capital actually issued to the shareholders.

3. Called up capital: Where only part of the amounts payable on each share has been asked for, the total amount asked for on all the shares is known as the called up capital.

4. Uncalled capital: This is the total amount which is to be received in future, but which has not yet been asked for.

5. Calls in arrears: The total amount for which payment has been asked but has not been paid by share holders.

6. Paid up capital: This is the total of the amount of share capital which has been actually paid by the shareholders.(Paid up capital = Called up capital – Calls in arrears)

Key points

1. Debentures- loan to the company from the public carrying fixed rate of interest.

2. Dividend: The profit that is being distributed to shareholders is called dividends.

3. Debenture interest: This is the interest paid on debentures to the debenture holders. This is an expense to be charged in the profit and loss account and if it owes it is known as a current liability in the balance sheet.

4. Ordinary shares: Shares entitled to dividend after the preference shareholders have been paid their dividends.

5. Preference shares: Shares that are entitled to an agreed rate of dividend before the ordinary shareholders receive anything.

6. Reserves: The transfer of apportioned profits to accounts for use in future.

7. Directors remunerations: This is the remuneration given to the directors and an expense to be shown in the profit and loss account.

8. Interim dividend: The dividend paid to the shareholders in between two annual general meetings.

It is shown in the profit & loss appropriation account only.

9. Proposed dividend: This dividend agreed by the board of directors but not paid. It is deducted from the profit & loss appropriation account and shown as a current liability in the balance sheet

10. Dividend is calculated on the paid up capital only.

11. For preference shares prefixed rate of dividend is paid.

E.g.: 7% Preference shares ----------------- rate of dividend is 7%

Therefore, preference dividend = Issued preference share capital x rate (%) / 100

12. For ordinary shares:

if dividend is paid as percentage of capital

Dividend = Issued ordinary share capital (nominal value) x rate (%) / 100

If dividend is payable per share:

Dividend = Number of ordinary issued shares x dividend per share

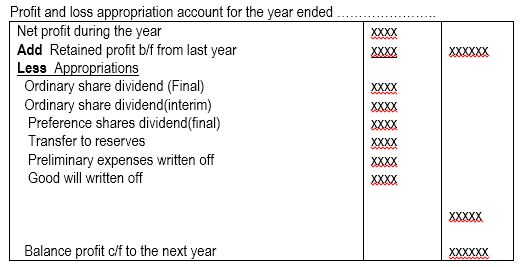

Profit and loss appropriation account.

This is the account prepared after the preparation of the trading and profit & loss account of a limited company. This account starts with the net profit obtained from the profit & loss account and the last year’s retained profit (if any). The appropriations of profits are shown in this account. After the appropriation, if there is any profit left over, it is called retained profit and it will be carried forward to the next year.

This is the account prepared after the preparation of the trading and profit & loss account of a limited company. This account starts with the net profit obtained from the profit & loss account and the last year’s retained profit (if any). The appropriations of profits are shown in this account. After the appropriation, if there is any profit left over, it is called retained profit and it will be carried forward to the next year.

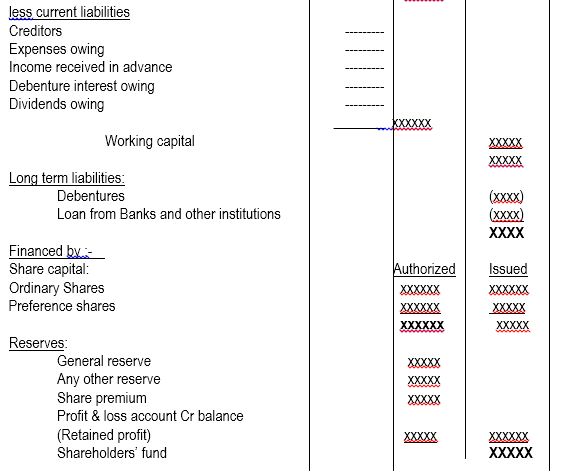

Format of balance sheet of a limited company