Accounts of non trading concerns

The business concerns are of two types: Trading concerns and non trading concerns.

Trading concerns are existing for the purpose of earning profit. But non trading concerns are existing for the purpose of rendering service to the public. E.g. of such concerns are clubs, societies, libraries etc. At the end of an accounting year the trading concerns prepare final accounts such as trading and profit and loss account and balance sheet. But non trading concerns prepare the following at the end of its accounting year:

The business concerns are of two types: Trading concerns and non trading concerns.

Trading concerns are existing for the purpose of earning profit. But non trading concerns are existing for the purpose of rendering service to the public. E.g. of such concerns are clubs, societies, libraries etc. At the end of an accounting year the trading concerns prepare final accounts such as trading and profit and loss account and balance sheet. But non trading concerns prepare the following at the end of its accounting year:

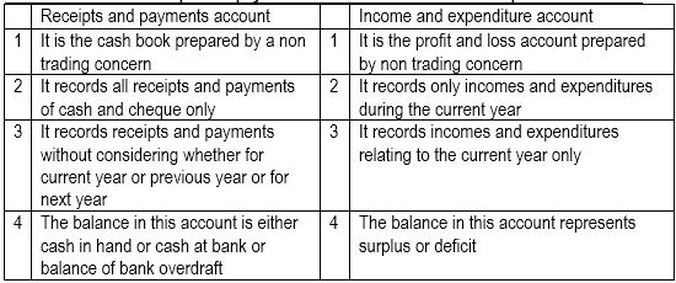

- Receipts and Payments accounts - it is summary of cash transactions of a non trading concern. It shows all receipts and payments during a year and the final balance of cash in hand or at bank or balance of bank overdraft. It is the cashbook prepared by a non trading concern.

- The income and expenditure account- this is similar to the profit and loss account prepared by a trading concern. It lists all the incomes and expenses of the non trading organization for a year. The result of this account is referred to as surplus or excess of income over expenditure or deficit or excess of expenditure over income. When the income is more than the expenditure the result is known as surplus. When the expenditure is more than the income, the result is known as deficit. It is prepared by considering all expenditures and incomes relating to the current year whether it is paid or not.

- Balance sheet- the balance sheet is prepared as in the case of a trading concern. But the excess of assets over liabilities of a non trading concern is known as accumulated fund. The surplus from income and expenditure account is added to and the deficit is deducted from accumulated fund.

Trading account Some non trading organizations do carry out regular trading activity, but this is not the main purpose of the organization. Many clubs and societies have a café, a shop, a bar and so on, where goods are bought and sold. A trading account should be prepared for each trading activity in order to calculate the gross profit or loss earned. The gross profit or loss of a trading activity of a non trading concern is transferred to the income and expenditure account. If it is gross profit, it is shown as income and if it is gross loss, shown as expenditure in the income and expenditure account.

Key points

Subscription received during the year + this year’s arrear + last year’s advance – last year’s arrear received – this year’s advance received for the next year

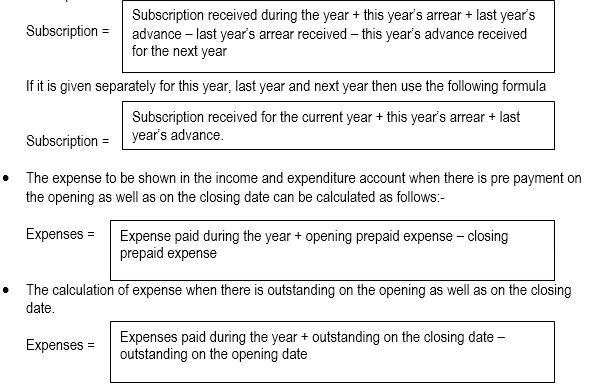

If it is given as a single amount, to find out the amount of subscription to be shown in the income and expenditure account, use the following formula:

Key points

- Accumulated fund on the opening date = total assets on the opening date – total liabilities on the opening date. It can be calculated by preparing an opening statement of affairs (balance sheet format) on the opening date, as a balancing figure.

- While preparing the trading account of bar or any other trading activity, if the purchase figure is not given, it can be calculated as:-

- The profit or loss as a result of sale of a fixed asset should be shown as income(if profit ) or expenditure( if loss) in the income and expenditure account.

- Usually the depreciation on fixed assets will be calculated by comparing the opening and closing values.

- The surplus is added with accumulated fund and deficit is deducted from accumulated fund.

- The stock items from trading activity are shown as current assets in the balance sheet.

- The subscription is one of the most important incomes for a non trading concern. It may be given as a single amount or separately for three years(for last year, this year and next year)

Subscription received during the year + this year’s arrear + last year’s advance – last year’s arrear received – this year’s advance received for the next year

If it is given as a single amount, to find out the amount of subscription to be shown in the income and expenditure account, use the following formula: