Bad debt and provision for bad debt

The amount of the debtors which cannot be recovered is known as bad debt. At the end the accounting year, the amount of bad debt is shown as an expense in the profit & loss account and deducted from the debtors. The double entry for recording the bad debt is:

Debit Bad debt account

Credit Debtors account

At the end of the year, while preparing the final accounts, the bad debt account is transferred to

the profit & loss account by passing the following adjustment entry:

Debit Profit & loss account

Credit Bad debt account

Provision for bad debt account or provision for doubtful debts account

The provision created to cover the next year’s bad debt expense out of the current year’s debtors

is known as provision for bad debts. This provision is created on the debtors after deducting the

current year’s bad debt. The double entries required for creating the provision for bad debt are:

First year Debit Profit & loss account and

Credit Provision for bad debts account.

Second year and subsequent years:

For an increase in the provision for bad debt:

Debit Profit & loss account and (with the amount increased)

Credit Provision for bad debts account.

For a decrease in the provision for bad debt:

Debit Provision for bad debt account and

Credit Profit & loss account

The amount of decrease in the provision for bad debt is shown as an income in the profit and loss account

While preparing the balance sheet, always the new provision for bad debt is deducted from the amount of debtors.

Provision for discount on debtors

This is the provision created to cover the expense of discount that may be allowed to the debtors during the coming year when they pay their debt on time. The increase in the provision for discount on debtors is also shown as an expense in the profit & loss account and the new provision for discount on debtors is deducted from the debtors in the balance sheet.

The amount of provision for decrease in the provision for discount on debtors is shown as an

income in the profit & loss account.

The double entries required for the provision for bad debt are:

During the first year to create the provision for discount on debtors:-

Profit & loss account Dr.

Provision for discount on debtors account Cr.

During the subsequent years, for an increase in the provision for discount on debtors:

Profit & loss account Dr.

Provisions for discount on debtors account Cr.

For a decrease in the provision for discount on debtors:

Provisions for discount on debtors account Dr.

Profit & loss account Cr.

Key points

Depreciation, Provision for depreciation and Asset disposal account

Depreciation is the part of the cost of the fixed asset consumed during its period of use by the business. In other words, it is the gradual reduction in the value of the fixed asset due to several reasons. Like other business expenses, depreciation is also a business expense to be charged to the profit & loss account at the end of every year.

Cases of depreciation

a. Wear and tear: Because of the regular usage in the business, the fixed assets eventually wear out.

b. Erosion, rust and decay: Erosion is subjected to asset like land, rust causes to the

asset like plant & machinery and decay is a process which will also be present due to the elements of nature and the lack of proper attention.

c. Obsolescence: This is the process of becoming out of date, then the value becomes less compared to the new and up-to-date equipment.

d. Inadequacy: This arises when an asset is no longer used because of the growth and changes in the size of the firm.

e. The time factors: This is applicable in the case of assets taken on the basis of lease.

When the years are finished the lease is worth nothing.

f. Depletion: This is applicable to the wasting assets like mines, quarries and oil wells.

According to the quantity of extraction of the raw material from the wasting asset, the

value remaining will be less.

Methods of calculating depreciation charges

Straight line method: This method is also known as fixed instalment method or original

cost method. Under this method, the cost of the asset (minus net residual value if any) is divided by the expected number of years of use of the asset.

Thus under this method, depreciation is =

Cost - estimated disposable value( residual value

Number of expected years of use

E.g.: A business bought a plant at a cost of $ 20 000, with an estimated life of 5 years and an estimated residual value of $ 2 000, the annual depreciation on this asset will be

20000 - 2000 = 3600 (every year)

5

Reducing balance method: Under this method, a fixed percentage of reduced balance

(cost less depreciation already charged )of the asset is calculated as depreciation at the end of every year. During the first year, the calculation will be made on the original cost

of the asset

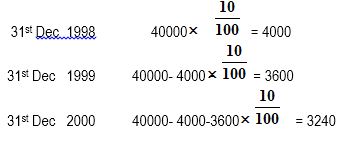

E.g.: An asset was bought for $ 40 000 on 1-1-1988. It was decided to charge the depreciation on this asset @ 10% under reducing balance method. The depreciation on this asset will be:

The amount of the debtors which cannot be recovered is known as bad debt. At the end the accounting year, the amount of bad debt is shown as an expense in the profit & loss account and deducted from the debtors. The double entry for recording the bad debt is:

Debit Bad debt account

Credit Debtors account

At the end of the year, while preparing the final accounts, the bad debt account is transferred to

the profit & loss account by passing the following adjustment entry:

Debit Profit & loss account

Credit Bad debt account

Provision for bad debt account or provision for doubtful debts account

The provision created to cover the next year’s bad debt expense out of the current year’s debtors

is known as provision for bad debts. This provision is created on the debtors after deducting the

current year’s bad debt. The double entries required for creating the provision for bad debt are:

First year Debit Profit & loss account and

Credit Provision for bad debts account.

Second year and subsequent years:

For an increase in the provision for bad debt:

Debit Profit & loss account and (with the amount increased)

Credit Provision for bad debts account.

For a decrease in the provision for bad debt:

Debit Provision for bad debt account and

Credit Profit & loss account

The amount of decrease in the provision for bad debt is shown as an income in the profit and loss account

While preparing the balance sheet, always the new provision for bad debt is deducted from the amount of debtors.

Provision for discount on debtors

This is the provision created to cover the expense of discount that may be allowed to the debtors during the coming year when they pay their debt on time. The increase in the provision for discount on debtors is also shown as an expense in the profit & loss account and the new provision for discount on debtors is deducted from the debtors in the balance sheet.

The amount of provision for decrease in the provision for discount on debtors is shown as an

income in the profit & loss account.

The double entries required for the provision for bad debt are:

During the first year to create the provision for discount on debtors:-

Profit & loss account Dr.

Provision for discount on debtors account Cr.

During the subsequent years, for an increase in the provision for discount on debtors:

Profit & loss account Dr.

Provisions for discount on debtors account Cr.

For a decrease in the provision for discount on debtors:

Provisions for discount on debtors account Dr.

Profit & loss account Cr.

Key points

- A debt written off is recorded in the books by debiting bad debts account and crediting debtors account.

- The provision for bad debt is calculated on the debtors’ balance obtained after deducting the bad debt written off.

- In the balance sheet, always the new provision for bad debt is deducted from the Debtors.

- Increase in the provision for bad debt is debited in the profit & loss account and credited in the provision for bad debt account.

- Decrease in the provision for bad debt is credited to profit & loss account and debited in the provision for bad debt account.

- Increase in the provision for bad debt is an expense and decrease in the provision for bad debt is an income to be shown to in the profit & loss account.

- The provision for discount on debtors is calculated on the debtors balance after deducting the bad debt and the provision for bad debt amount.

- Always new provision for discount on debtors is deducted from debtors, after deducting the provision for bad debt.

- Increase in the provision for discount on debtors is debited to profit & loss account and credited to provision for discount on debtors account.

- Decrease in the provision for bad debt is debited to provision for discount on debtors account and credited to profit & loss account.

- Increase in the provision for discount on debtors is an expense and decrease in the provision for discount on debtors is an income to be shown in the profit & loss account.

Depreciation, Provision for depreciation and Asset disposal account

Depreciation is the part of the cost of the fixed asset consumed during its period of use by the business. In other words, it is the gradual reduction in the value of the fixed asset due to several reasons. Like other business expenses, depreciation is also a business expense to be charged to the profit & loss account at the end of every year.

Cases of depreciation

a. Wear and tear: Because of the regular usage in the business, the fixed assets eventually wear out.

b. Erosion, rust and decay: Erosion is subjected to asset like land, rust causes to the

asset like plant & machinery and decay is a process which will also be present due to the elements of nature and the lack of proper attention.

c. Obsolescence: This is the process of becoming out of date, then the value becomes less compared to the new and up-to-date equipment.

d. Inadequacy: This arises when an asset is no longer used because of the growth and changes in the size of the firm.

e. The time factors: This is applicable in the case of assets taken on the basis of lease.

When the years are finished the lease is worth nothing.

f. Depletion: This is applicable to the wasting assets like mines, quarries and oil wells.

According to the quantity of extraction of the raw material from the wasting asset, the

value remaining will be less.

Methods of calculating depreciation charges

Straight line method: This method is also known as fixed instalment method or original

cost method. Under this method, the cost of the asset (minus net residual value if any) is divided by the expected number of years of use of the asset.

Thus under this method, depreciation is =

Cost - estimated disposable value( residual value

Number of expected years of use

E.g.: A business bought a plant at a cost of $ 20 000, with an estimated life of 5 years and an estimated residual value of $ 2 000, the annual depreciation on this asset will be

20000 - 2000 = 3600 (every year)

5

Reducing balance method: Under this method, a fixed percentage of reduced balance

(cost less depreciation already charged )of the asset is calculated as depreciation at the end of every year. During the first year, the calculation will be made on the original cost

of the asset

E.g.: An asset was bought for $ 40 000 on 1-1-1988. It was decided to charge the depreciation on this asset @ 10% under reducing balance method. The depreciation on this asset will be:

Thus under this method, the yearly depreciation will be reducing year after year. But in

the case of fixed instalment method, the amount of depreciation will be fixed or same every year.

Revaluation method: Under this method, the depreciation is calculated by comparing

the opening and closing values of the asset. The difference between these values will

be taken as the amount of depreciation during that year. This method is suitable for the

assets like small tools, screwdrivers, spanners etc.

Residual value: This is the value that the business will get from the sale of an asset at

the end of its useful life time. It is also known as scrap value or salvage value

Provision for depreciation

This is the provision created to cover the expense of depreciation on fixed assets. Every year the amount of depreciation is credited to this account and debited to the profit & loss account.

The depreciation amount will accumulate year after year. At the end of the life of the asset or at the time sale of the asset, the accumulated depreciation is transferred to the asset account or the asset disposal account. At the end of every year, the balance in the provision for depreciation is shown as a deduction from the cost price of the concerned asset.

The double entry for creating the provision for depreciation is:

Profit & loss account Dr.

Provision for depreciation account Cr.

Disposal of an asset

When an asset is sold, the procedure will recorded in a separate account called asset disposal account. The following double entries are required for recording these transactions in the books of the business:

1. For transferring the cost price of the asset sold to the asset disposal account

Asset disposal account Dr

Asset account Cr.

2. For transferring the provision for depreciation already charged on the asset sold from the provision for depreciation account to the asset disposal account:

Provision for depreciation account Dr.

Asset disposal account Cr.

3. For recording the cash or cheque received from the sale of the asset:

Cash / Cheque Dr.

Asset disposal account Cr.

4. To record the profit on sale of the asset:

Asset disposal account Dr.

Profit & Loss account Cr.

5. To record the loss on sale of the asset:

Profit & loss account Dr.

Asset disposal account Cr

Key points

the case of fixed instalment method, the amount of depreciation will be fixed or same every year.

Revaluation method: Under this method, the depreciation is calculated by comparing

the opening and closing values of the asset. The difference between these values will

be taken as the amount of depreciation during that year. This method is suitable for the

assets like small tools, screwdrivers, spanners etc.

Residual value: This is the value that the business will get from the sale of an asset at

the end of its useful life time. It is also known as scrap value or salvage value

Provision for depreciation

This is the provision created to cover the expense of depreciation on fixed assets. Every year the amount of depreciation is credited to this account and debited to the profit & loss account.

The depreciation amount will accumulate year after year. At the end of the life of the asset or at the time sale of the asset, the accumulated depreciation is transferred to the asset account or the asset disposal account. At the end of every year, the balance in the provision for depreciation is shown as a deduction from the cost price of the concerned asset.

The double entry for creating the provision for depreciation is:

Profit & loss account Dr.

Provision for depreciation account Cr.

Disposal of an asset

When an asset is sold, the procedure will recorded in a separate account called asset disposal account. The following double entries are required for recording these transactions in the books of the business:

1. For transferring the cost price of the asset sold to the asset disposal account

Asset disposal account Dr

Asset account Cr.

2. For transferring the provision for depreciation already charged on the asset sold from the provision for depreciation account to the asset disposal account:

Provision for depreciation account Dr.

Asset disposal account Cr.

3. For recording the cash or cheque received from the sale of the asset:

Cash / Cheque Dr.

Asset disposal account Cr.

4. To record the profit on sale of the asset:

Asset disposal account Dr.

Profit & Loss account Cr.

5. To record the loss on sale of the asset:

Profit & loss account Dr.

Asset disposal account Cr

Key points

- Profit / loss on sale of asset = (Sale proceeds of assets + provision for depreciation to date) – Cost price of the asset sold.

- Under straight line method, the value of asset will be reduced to zero or the scrap value at the end of its useful life.

- Under the reducing balance method the amount of depreciation reduces year after year.

- Profit on sale of asset is credited to the profit & loss account

- Loss on sale of asset is debited to the profit & loss account.